Austin Real Estate Market Overview

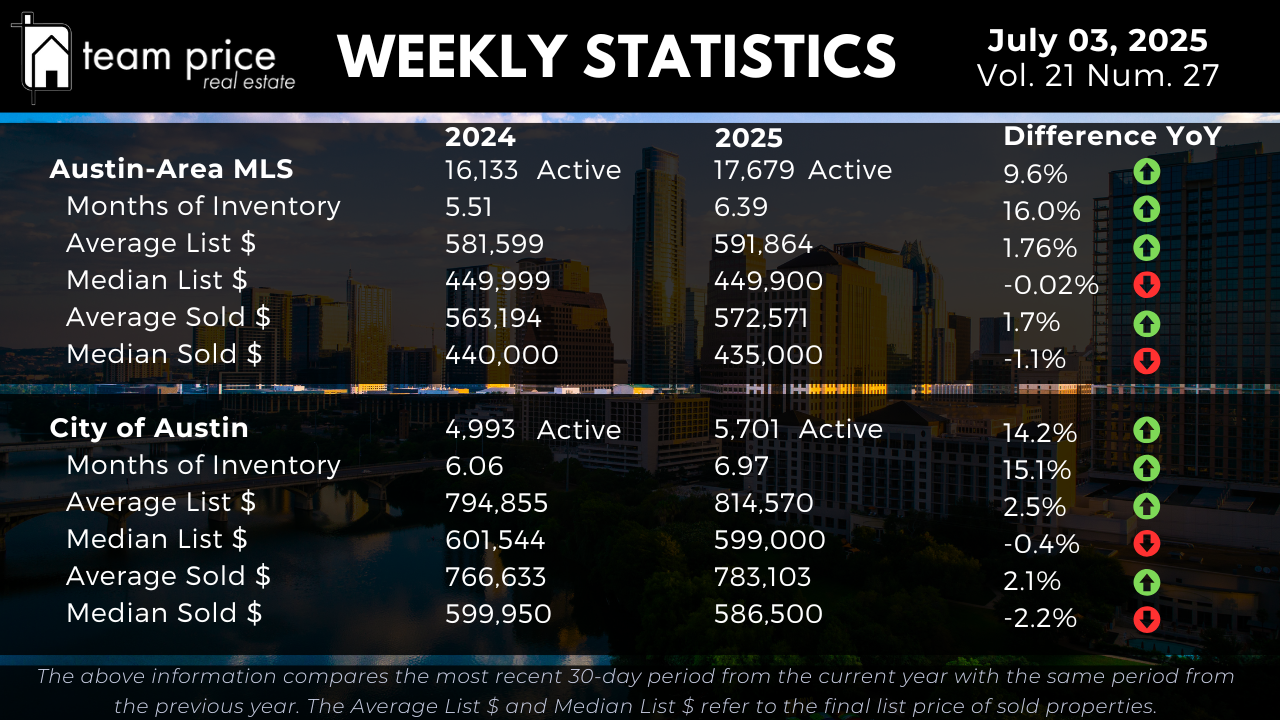

Inventory levels across the Austin-Area MLS continue their steady upward climb, signaling that the region remains firmly in a market transition phase. As of this week, there are 17,679 active residential listings on the market, up 9.6% from the same period last year. Months of Inventory has expanded to 6.39, a 16.0% year-over-year increase that reflects the consistent buildup of supply and a more deliberate pace of buyer activity. Within the City of Austin, these inventory trends are even more evident. Active listings have increased by 14.2%, rising from 4,993 to 5,701 homes. Months of Inventory has grown from 6.06 to 6.97, a 15.1% rise that further confirms the growing leverage available to buyers as sellers adjust expectations. The region’s supply trends suggest sellers face increased competition, while buyers enjoy more options, greater negotiating room, and fewer bidding wars compared to recent years.

Austin Housing Prices: Stability with Pockets of Softness

The latest pricing data reflects a market in a delicate balancing act between buyer caution and seller confidence. Across the Austin-Area MLS, the average list price for active homes now sits at $591,864, a modest 1.76% increase compared to last year. The median list price remains virtually unchanged, down just 0.02% to $449,900. On the sales side, average sold prices have ticked up by 1.7% year over year to $572,571, while the median sold price has softened slightly, declining 1.1% to $435,000. This dynamic suggests that while upper-tier properties are helping to buoy average prices, middle-market and entry-level segments are experiencing pricing pressure as affordability remains top of mind for many buyers.

Within Austin city limits, the market shows a similar but more pronounced divide. The average list price has increased 2.5% year over year to $814,570, highlighting continued strength in the luxury and higher-end segments. Conversely, the median list price has dipped 0.4% to $599,000, pointing to increased price sensitivity and competition among mid-range homes. Average sold prices in Austin are up 2.1% to $783,103, yet median sold prices have fallen 2.2% to $586,500. These figures underscore a familiar theme: while well-located, higher-end properties retain buyer attention, affordability challenges and inventory growth continue to weigh on broader pricing, particularly for homes in the $500,000 to $600,000 range.

Regional Trends: Correction Persists Across Central Texas

Across the 30 cities tracked in Central Texas, market conditions remain mixed, with no clear signs of sustained price recovery. Half of those cities—15 out of 30—posted month-over-month price increases, while the other half experienced declines. The longer-term view, however, reveals broader weakness. Just 37% of cities recorded year-over-year price gains, while 63% saw prices fall. Notably, none of these cities remain above their pricing peak from the past 12 months, reflecting the continued, region-wide market correction.

A similar pattern is playing out at the ZIP code level. Of the 75 ZIP codes monitored, 45% posted month-over-month price increases, while 53% experienced declines. On a year-over-year basis, only 37% of ZIP codes have seen price growth, with the remaining 63% reflecting price declines. Just one ZIP code across the region remains above its 12-month pricing peak, further confirming that the correction remains broad-based, despite isolated signs of monthly improvement in some submarkets.

List-to-Sale Price Performance: Negotiation Remains the Norm

Price negotiations continue to define the current market environment. So far this month, 65.71% of all homes sold in the Austin-area MLS closed below their original list price, a slight increase from last month’s 62.80% and notably higher than the 63.42% recorded this time last year. An additional 21.87% of sales closed precisely at list price, while only 12.43% of properties sold above asking—a decline from both last month and June of 2024. The average sold-to-list price ratio now stands at 97.27%, reinforcing that while many homes are still trading near asking price, the majority of sellers are making modest concessions to secure buyers. Homes priced appropriately and marketed effectively continue to draw interest, but buyers are increasingly strategic and selective, particularly in the face of expanding inventory.

Peak Value Trends: Market Remains Well Below Previous Highs

Despite relative stability over the past few months, the broader Austin housing market remains well below its previous peak pricing. In the Austin-Area MLS, the average list price peaked at $715,542 in April 2025 and has since declined to $657,192, marking an 8.2% drop. The median list price is down 12.0% from its May 2022 peak of $539,900 to $475,000. Similarly, the average sold price has fallen 13.7% from its May 2022 high of $664,515 to $573,723, while the median sold price has retreated nearly 20%, dropping from $538,000 to $431,000. Price per square foot figures reflect comparable declines, with averages down over 20% from their peaks.

The City of Austin has followed the same trajectory. The average list price, once as high as $949,938 in April 2025, now stands at $834,581, a 12.1% decrease. The median list price has fallen 12.3% from $661,250 to $579,950. The average sold price has slipped 7.1% from its $847,583 peak to $787,052, while the median sold price is down 13.8% to $586,000. Price per square foot declines in Austin have also been significant, with the median figure down more than 20% from its peak of $393 to $311. These figures confirm that while some pricing stability has returned, the broader market remains well below its highs from 2022 and early 2025, signaling an extended correction cycle that continues to shape buyer and seller expectations alike.